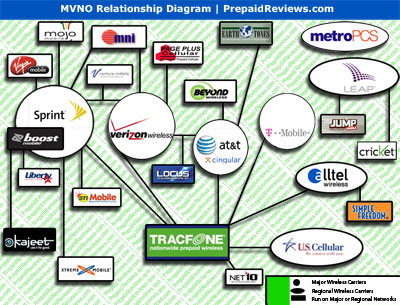

MVNOs have sunk in the past 18 months, and a number of others, including Virgin Mobile and Helio aren’t performing as well as they had hoped. Yet we see new MVNOs pop up around the world, and don’t hear the same stories of their failure. Why is this? How can MVNOs succeed in one environment, and not another? Once again, we might not be able to solidly conclude the answer, but we can take a look at what some people have to say on the issue.

Issues of competition

Shooting themselves in the foot

The more I think about it, the more I understand why Amp’d Mobile tanked. Look at the service they were offering. It was a media-rich mobile experience which targeted a higher-end user base. And, at the same time, it targeted youths, who have the most draw to these media functions. On the youth end, Virgin and Boost had a good corner on the market. True, Amp’d could have come in with a superior service and succeeded that way. The problem is that they priced their services out of the reach of most teenagers. The other problem, of course, is that the major operators have been figuring out this media thing pretty quickly. High end users have a great number of options when it comes to media on their phones — to the point where they don’t need to trust an unknown brand with their cell service (yes, branding probably worked against Amp’d). So, basically, Amp’d targeted audiences which were pretty much covered already. They failed to differentiate themselves at the outset, though that is quite a difficult task. Verizon, one of their biggest creditors, saw the clear competition between the two, and decided to call in the debt, which it knew Amp’d could not repay. And there went an MVNO.Confusing plans

Some MVNOs simply offer too many options, which become confusing. Look at Locus prepaid. They offer a number of plans that can fit the budgets of many people. However, if you offer people too many options, it will just become information overload. Unable to decipher which deal is best, they will walk away to another company. An excellent example of this is Movida, which filed for bankruptcy in early April, and were bought up by the end of the month. Just look at their rates page. It takes some calculating to figure out what plan works best with your calling habits. True, Virgin Mobile offers a number of options for its pay as you go customers, but they offer assistance in figuring out what plan is best for you. That is a boon to the consumer. They can figure out how much they talk a month, and pick a plan with assistance from Virgin Mobile. There is no such assistance from Movida, or really any other MVNO I can think of. You don’t have to tread the customer like an idiot; you just have to make everything clear, including the specific advantages of each of your offerings.The problem will work itself out

On questions of MVNOs, the first place to look is to Alex Besen, founder of The Besen Group, an MVNO consultant. He might not have the answer, but he can certainly offer a high level of insight. And he thinks that this is a temporary problem. Currently, MVNOs only comprise seven percent of mobile users in the U.S. Clearly, that number will have to go up if we’re going to see more than three or four MVNOs succeed. What is it going to take to see any increase? A greater level of market saturation, says Besen. The U.S. is projected to see a near-100 percent saturation in three years. This, says Besen, will spur a growth in MVNOs, likely giving them up to 17 percent of the market. This will mean room for more MVNOs, and more importantly, more MVNOs to succeed. Besen believes that once we hit this level of saturation, MVNOs will become an asset to carriers. It will help them lure people away from other carriers. Having a youth-based MVNO, like kajeet, will allow companies to pick up the new entrants to the market at the earliest possible stage. And their offering of niche MVNOs will help keep them around. The overall point is that we cannot discount this MVNO business model, which has worked elsewhere in the world, just because a few have failed. When you have a gold rush mentality, clearly there are going to be those who don’t make the grade. So once the dust settles, and the saturation rate rises, we should see a number of MVNOs become successful in the United States.]]>

Posted in MVNO

MVNOs in general need to offer better texting plans if they want to capture the younger market. Only one provider offer bundles, virgin mobile, and that is what you see most teens and young adults having when it comes to mnvo services. In fact, I wouldn’t be surprised if texting bundles are the only reason why Virgin is afloat.

Something that is often overlooked in the failure of many MVNOs is their network deal. Virgin Mobile was a joint venture with Sprint where both companies succeeded when they created a valuable company, rather than a traditional arms-length wholesale partnership. Boost was similar in its original deal with Nextel.

Anyone who has been in the industry for a while remembers that many “resellers” (some of them big names like MCI) got out of the business in the late 1990s because there was no margin. Somehow, content companies thought they could do it differently, but they failed to get the network deal that support carrier-like economics.

I agree that we are likely to find new iterations of companies partnering with the big networks in the US, but it won’t be a reseller model.

I am not sure why this article or many other such articles dont refer to two things:

1. US market is probably one of the only major markets where operators offer branded handsets (at least as of 2007/8). All of the major MVNOs – Virgin, Amp’d, Helio and others offer branded handsets with customized features. The cost of acquisition of a customer goes up because of the subsidy that they need to offer on these handsets. Add to this distribution cost and the retailer bounty, the break-even on a new customer becomes an uphill task. Additionally, these MVNOs cannot command the handset volumes to match the top service providers and hence cannot demand better pricing from the handset manufacturers.

2. There is still lack of a ‘unique’ value proposition which can be refreshed on a regular basis by these MVNOs. In this competitive environment, the big operators are ceating value offers for all customer segments. Their prepaid plans are comparable if not better than what are offered by the MVNOs. On the high end, all of the US operators have brought out ‘all you can eat’ voice and data plans to the market.

In the future, the market might improve for the MVNOs but until then sustainability is going to be key. Regardless, competing with your suppliers is a tough place to be.

One thing that is contradictory is that your first section titled “Issues of Competition” rationally explains how as the US market reaches cell phone handset saturation, the major carriers start to compete with the MVNOs. This makes sense.

Then in your closing sections, you say that the opportunity for MVNOs will grow. “What’s it gonna take? A greater level of market saturation, says Besen.”

That’s totally contradictory. Furthermore, I would agree more with the former argument than the latter. The MVNO’s ability to differentiate was high while the majors had a “Ford Model T” strategy for cellular service. But as the markets get more competitive, and the land grab days of easy customer adds goes away, the carriers need to focus more on customer niches, flexible plans, segmentation strategies, variety of options, etc. This additional competition will increase the challenges of MVNOs.

At this juncture, the best bet for an MVNO is to stake out a demographic, win subscribers in numbers > 750,000 and await a buyout from a major carrier or PR. But getting subs > 500k has proven elusive to MVNOs, and at that scale, you burn money and are of little interest as a M&A target.

Derek Kerton

http://www.kertongroup.com